The financial services industry has entered 2018 with a focus on digitizing services to better meet customers’ needs. But do the banks understand that previously inefficient, paper-based processes and messy ‘not so friendly’ user interfaces are no longer going to be good enough in today’s technologically advanced environment?

Banks are needed to connect digitally to succeed. With FinTech continuing to gain momentum, it’s just a matter of time, to see them fully integrated into business-as-usual banking.

One of the world’s largest Deutsche bank calls for “a shift in mindset from one of competition to collaboration,” arguing that traditional banking providers and new innovators must work together in order to revolutionize the payments market and the wider financial sector for the benefit of all.

They said it and I quote:

“For both parties, a partnership should liberate them to focus on their core competencies and contribute these areas of expertise to the innovation process.”

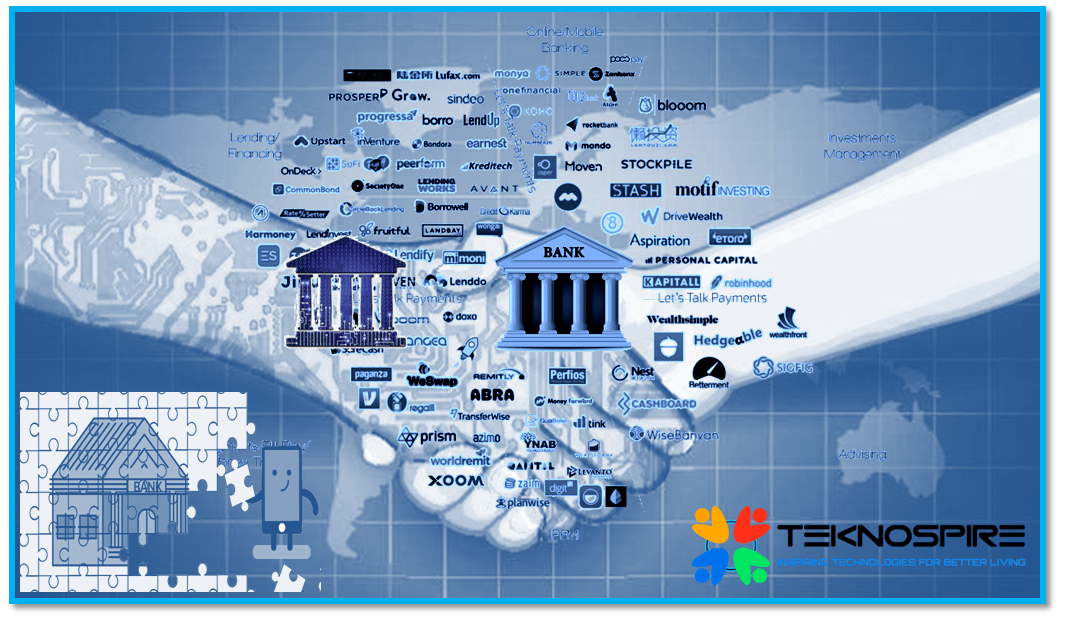

Fintech, no doubt, is the talk of the day amongst investors, financial service providers, entrepreneurs, and even big corporate houses. The phenomenal potential of creating innovative services and business model makes it disruptive in nature. Realizing the immense potential of the technology, “Banks” are looking to integrate with FinTech solutions.

In short Bank+FinTech merger is next on the cards in the coming years.

Welcome to the Era of FinTech.

FinTech Nudged All

FinTech, the technological innovation in the financial arena, registered its birth as a back-end activity, and today is nudging everything across the globe. It has transformed, almost everything, in such a way that you are about to witness the impact of the “fourth industrial revolution”.

More than anything, it has created its own “FinTech Ecosystem” by embracing the following:

FinTech has impressed the Banking Sector and its customers, which is why the transformation in banking has touched a new height. The “2016 World Retail Banking Report” states that almost two-thirds of the retail banking customers across the world use FinTech products or services like cards & payments, loans, Investments, financial advice and mortgages.

This is because of the UX standards they offer to their customers. 81% of the customers feel that FinTech offers faster services and extends a great experience.

In addition, FinTech firms are fast catching up bank’s “niche parameter”- TRUST. The percent of customers who have complete or partial trust in FinTech firms is as high as 87.9% across the globe.

FinTech-Globally Embraced

Global acceptance of FinTech is evident from a recent comparative study by EY (formerly Ernst and Young) which reported FinTech adoption between 2015 and 2017 has increased across various countries like- Australia, France, Germany, China, and India. The figures indicate adoption of past (2015), present (2017), and future (as responded in the survey).

(Image credit: EY)

The adoption of FinTech in these countries has climbed exponentially:

- Australia- From 13% in 2015 to 37% in 2017

- France- From 27% in 2015 to 40% in 2017

- Germany- From 12% in 2015 to 35% in 2017

- China – From 69% in 2015 to 77% in 2017

- India – From 52% in 2015 to 80% in 2017

‘Banking with FinTech’ attraction

Like any other sector, Banks have started reacting to FinTech, and since 2015, FinTech Banks have started emerging. Banks and Financial inclusions have initiated startup programs to constitute FinTech companies. Across the globe, 43% banks created such startups. Another 20% set up VCs to fund FinTechs. There are obvious reasons behind banks being forced to or influenced by FinTechs.

EY FinTech Adoption Index 2017 released in June 2017 indicates that the appetite of digitally active consumers has risen considerably, from just one in seven digitally active consumers in 2015 to one in three in 2017. The report also shows that in 2017, there are 84% consumers aware of the fintech facilities in comparison to just 62% in 2015. The same reports show that the fintech adoption rate is expected to reach an average of 52% globally from the current rate of 33% in 2017.

Such growth in numbers could soon blur the boundaries between different financial services, laying down new standards for the industry during the process. To stay ahead of the curve, financial firms would benefit from the technical assistance from the fintech startups.

Why FinTech Lures Banks

Unlike traditional banking,

by the World Retail Banking Report 2016

The fast and efficient products and services of FinTech have attracted Banks to offer P2B services. This is evident from the fact that many have started offering traditional in-bank services on mobile devices as well. This has helped them offer high levels of access to consumer, and hence, a better usability and User Experience (UX) standards.

Advantages of the Alliance between

FinTech and Banks

With FinTech and Bank partnership, the ultimate beneficiary will be the consumer. Banks can utilize technology to shift their focal point from “Bank” to “Banking” and, in return, offer customers independence from standard products or services, freedom to choose amongst the best and better ‘Digital Banking’ Experience.

Collaborating, instead of competing, with startups can provide fresh tech solutions for banks. Banks, together with FinTech, with shared services and knowledge, can leverage the abundance of information available in “Big Data” by using data analytics tools like Predictive Analytics and gain an enhanced understanding of the customers thereby offering deeper engagements by offering:

- Customized products

- Comprehensive services.

They can unleash the potential of FinTech in banking to evaluate, identify, and create products or distinctive services/ solutions for consumers demand and sometimes even before the customer realizes.

Collaborations will provide the perfect opportunity to leverage the full potential of the technology and will allow the banks to meet the demand of digitally savvy users which will immensely get benefitted from this association, as:

- Services and information will freely flow between banks to customers,

- It’ll skip the traditional needs of teller windows or counters,

- Financial management of customers will be simplified, and

- The integration of account and payment information will happen in the form of mobile apps – ‘Bank – always on a go’.

It’s a Win-Win situation for startups also. Collaboration with banks and financial institutions will provide access to funds. Many young companies have to look towards business incubators and VCs, which have their own challenges. And, also, there are not many people who understand financial markets and how to create technology-based solutions that will actually be adopted.

Digital solutions are so widespread that creating a unique value proposition can be as much of a challenge as developing the financial technology itself. This creates a unique environment for competitive companies.

Financial technology companies also face the challenge of “technology” itself. With new much smarter, faster and more secure devices/technologies ‘pouring in’ frequently, it is also for startups, who will need more funds, first to constantly update themselves and then to provide unique solutions to cater that demand in the market ‘to stay ahead’.

That, with focus on ‘customer centric’, both should support each other and grow together in a strong, scalable and sustainable run, is the ‘need of the hour’.

Hence, they must collaborate with security measures, authentication processes, and cyber security measures to build a distinct bond between the two.

The common belief that FinTech will disrupt banking is a myth, competition – not collaboration will be the primary driver of disruption. Through collaborations, fintech startups and banks can have access to broader markets, along with a number of other benefits.

According to Matt Hatch, partner and Americas FinTech Leader at EY:

“In the year 2016, the average return on equity (ROE) for the largest 200 global banks was just over 7.1%. Banks can increase their ROE by collaborating with fintech [companies], which has the joint benefit of driving down cost while accelerating innovation”.

“Taking the first step is often difficult because of a general reluctance to change – even when there is an appetite to be a part of an innovative, cutting-edge organization. Before embarking on this journey, make sure your ducks are in a row. First, look internally at current systems and offerings. Then ask – how can we use fintech partnerships to enhance what we currently have in place? Over time, integrate innovation as a central part of your growth strategy.”

Collaboration – not competition is the key. It is highly predicted that the consolidation will be successful, as together they can offer customers a holistic service or product, which will increase the customer satisfaction, loyalty, and certainly, revenue. Banks must adapt to global digitalization quickly, and evolve, learning quickly from the void and disruption caused by innovation.

With the clock ticking every second, banks and FinTechs should ‘welcome each other with open arms’, to provide unmatched UI/UX services and products, to welcome customers, new and old, and more importantly, protect their own grounds.

References:

- https://teknospire.com/

- https://www.i-scoop.eu/fintech/

- https://technode.com/2017/09/01/china-india-fintech/

- https://www.worldretailbankingreport.com/#world-retail-banking-report-2016

- Creative 1

- Creative 2

- https://centricdigital.com/blog/digital-transformation/fintech-and-innovation-in-traditional-banking/