The world is under the spell of digitization! Just a decade back, when people were skeptical about making a transaction online, the recent reports are highlighting the mass adoption of technology into their lives. Sample these –

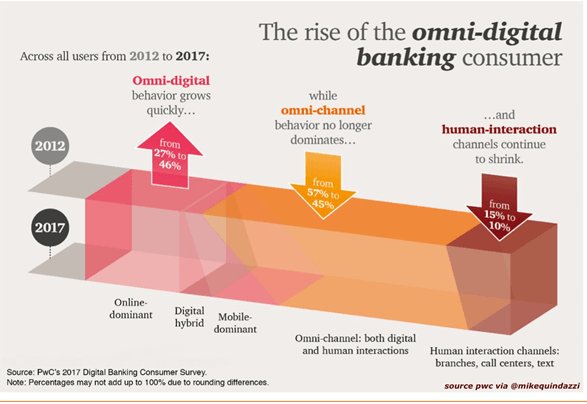

Image Source – PWC 2017

Such a massive growth is a collaborative effort of fintech firms and banks.

So, could we say Digital Banking is dependent on fintech firms? Or Are banks dependant on their technology providers? Could we in future see banks more like regulators and fintech firms as an operating wing? With concepts like branchless banking, contactless banking evolving would bank be merged? Do we foresee fintech firm expansion that results in bypassing banks? To answer many such questions, we decided to come up with this post.

Banks and fintech firms

In layman terms – any of the banking services/activities when availed via digital/electronic mode is referred to as Digital banking. So, if you are using your e-wallet or logged in to your bank website for funds transfer or online shopping. In fact for banks like e-KYC or automation of opening a bank account are also some of the examples of digital banking.

In India, as per 2017 Oracle J.D. Power India Retail Banking Study , 94% of retail banking customers have visited the branch/store at least once in the past 12 months that signifies how services are availed via digital means. Only 51% of retail banking customers have a reliable online banking experience with their primary financial institution.

While individuals specified concern of security as the prime reason for non-usage of digital channels. The most surprising fact highlighted in the study was – ~94% of urban customer prefer to visit a branch to avail banking services indicating lack of trust on digital channels.

While these are the stats lets check on health meter of banks and fintech firm and their contribution towards Digital banking.

Well, that’s our present situation! Banks and fintech and not competing with each other, there is no overlap. Banks are learning to adapt to digitization and fintech firms are providing solutions to make banker and their customer’s life easier. Traditional banking processes are evolving as now people have an option of

So Bank needs to offer the traditional products but also adopt the modern ways of handling money, that’s why they need fintech.

On the other hand, fintech firms have hands-on experience on latest technology but to build a customer base, to build the trust, to get accredited by regulatory authorities they need to prove their worth. Hence they need banks. Both entities need each other to progress – strengthen their customer base, build customer’s trust and outgrow their competition.

As per a report from CBinsights , these 78 India based fintech start-ups are building the ecosystem to support Digital India move. While the solutions are offered under various categories like Payments, Lending, Insurance, Trading platform, and taxes, experts believe that simplified yet intuitive UX designing has led fintech firms to gain customers attention and win loyalty.

Banks and fintech firms

Many fintech firms like Teknospire or ElectronicPay collaborates with Banks to use their fintech solution for better transparency and growth of their client. Other businesses like FundsIndia or NukkadShop or Veritas Finance directly deal with their clients acting as a mediator between banks and customers.

In short, we could say that currently the banks and fintech firms are working in parallel lines to accumulate a rich customer base, penetrate in every nook and corner of India. While this seems to be a healthy competition but what happens when you have achieved all that and established yourself as a brand? What happens when your product is significant, but you are not able to reach out to the mass? A merger or an acquisition? Only time can tell.

One of the recent articles on economic timese read – In the match for India’s financial services future, fintech just scored twice while banks are still struggling to retrieve the ball they scuffed into their net. While ET predicted [based on facts] that fintech would lead and banks would be slaughtered by them, let’s quickly glance other facts –

That’s the hard reality, despite traditional institutions[banks] juggling between modern and old approach, they[banks] are still the first choice of HNIs and corporate offices. You pick any office across India, none of them [corporate accounts] yet have an account [ because of the regulatory constraints] with fintech firms. Be it crediting salary to your employees or managing your business financial portfolio banks are still the preferred choice.

Search a term on google, and it would show you the result of location, contact numbers, and review. With such an ease of availing services at the urban location, residents find it easy to encash offers and convenience provided by fintech firms. However, tier2 cities and specifically remote areas are untouched by this handiness. Hence banks may again be a preferred choice for people in rural areas.

As you approach a branchless bank, you are greeted by a robot who ask you your account number, with your biometrics valid authentication, he/she then ask- How could I help you? Or how about your smartphone fintech app with google cardboard allowing you to connect to your virtual bank from your home and get query resolved. If yes, we do see banks being redundant.

Banks have mandatory guidelines/tests conducted before offering employment to any individual. Could the solutions offered by fintech firms be certified against such criteria? Could a software be marked as Regulatory checked from Reserve Bank of India? In fact, FinTech Firms or NBFC that are inclined to offer banking cadre services would need to get regulatory clearance before doing so. So that RBI grades them, and then the start operating /deploying software for NBFC.

Well, the debate could go on and on but what is vital is to understand the process of evolution. The change that is happening now! Technology is disrupting the way we see banking and only time can tell who is made redundant, but the good part is the progression of Digital Wave… Digital banking… banking to All and Financial Inclusion – that’s the way to step into the future!

Teknospire with its banking solution like Agent Banking Solutions , Mobile Money product and Payment Switch is helping banks in rural and remote areas to offer digitize services to farmers, local business owners and government employees. For more information please contact us here

References:

Why Is India Lagging In Its Digital Banking Efforts?

The India Fintech Market Map: 72 Startups Working Across Lending, Payments, Insurance & Banking

At this rate, Fintech will slaughter India’s banks

Fintech’s Coming to Trounce India’s Banks