Preamble

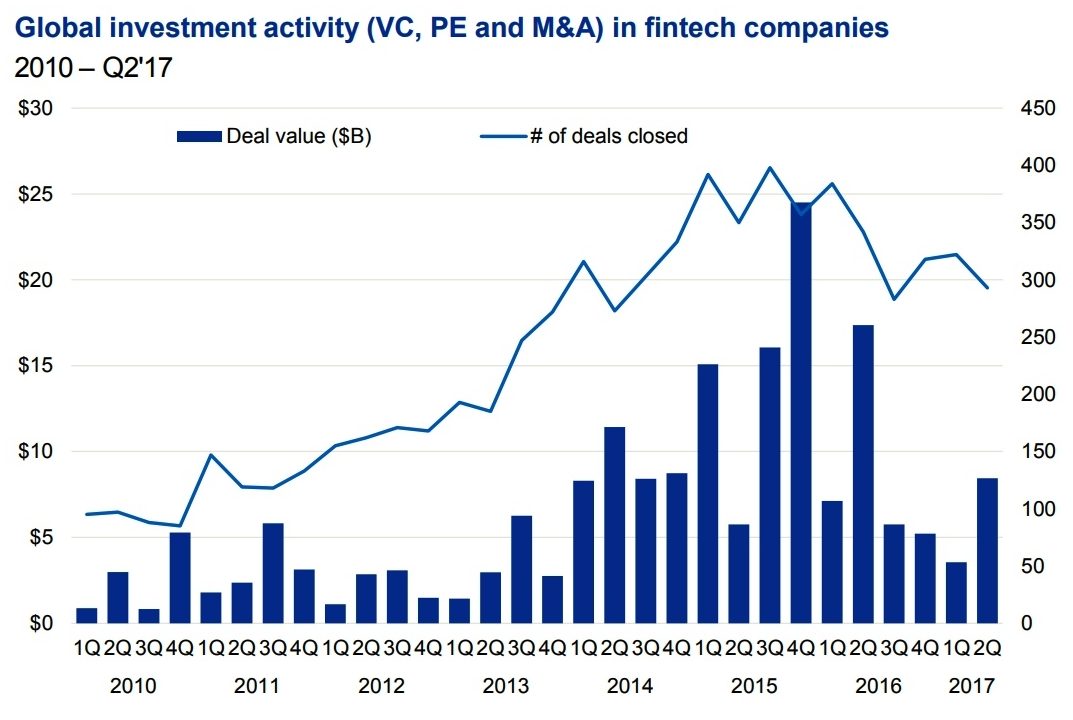

The global Fintech trends show an investment of £25.6bn in 2015 rising to £27bn by 2016.

Source: kpmg.com

The global Fintech investments doubled in the period ending Q2 ’17 and reached $8.4billion.

Similarly, in the period ending Q4 ’17, the figure was $8.7billion across 307 deals with annual global Fintech investment touching $31billion in 2017.

FINTECH ASIA

Asia probably “knows the way, goes the way, and definitely shows the way” and hence, is leading the globe in Fintech, fast embracing the innovation, adoption, and attending the unaddressed Asian customer needs.

Asia Statistics for fintech companies

Source: kpmg.com

Fintech has seen some incredible growth around the world. According to DBS CIO Neal Cross, and I quote :

“Asia is the real “waking giant” on the scene. Late to the party but catching up fast.”

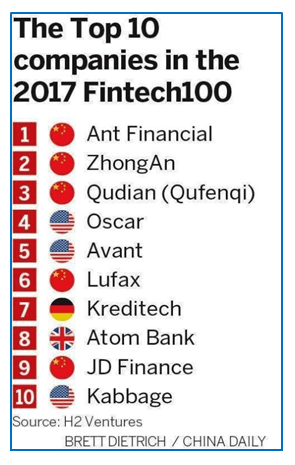

The fact that of the top ten leading Fintech companies in the world, five (Ant Financial, Qudian, Lufax, ZhongAn, and JD Finance) are from People’s Republic of China (Asia) is enough to justify the lead.

Source : Top 10 FinTech Companies in 2017

Though the primary focal point of Fintech companies has been customer-based initiatives (B2C) and customer experience, it seems they have started believing in “ignore the noise and focus on the work”; hence, have shifted their focus to B2B solutions. In the period ending Q2’17, it is reported that out of the top 10 Fintech global deals, three are B2B-focused companies namely- CCH Tagetik ($321m), Pos Portal ($158m), and ITRS Group ($140.6m).

Trends Which Keep Asia Leading the Fintech B2B and B2C Solutions

The legend “Only a king can attract a queen and only a queen can keep a King focused” stands true for Asian Fintech markets.

The King of global Fintech- Asia has been attracting a lot of investments in the recent past which is evident from the Fintech trends in 2016, of the £27bn global investment £11.7bn was done in Asia, a whopping 44% share.

Leading the region, China is estimated to have done an investment of $10bn in 2016 followed by India which did a Fintech investment of $1.1bn Fintech investment.

Source : The Fintech Times May12,2017

Apart from these two major countries, other countries like Thailand, Cambodia, Myanmar, Malaysia, Indonesia, and the Philippines did a cumulative investment of $217mn in 2016.

Singapore and Hong Kong clocked $800mn with $400mn each, which experts feel is a clear financial prediction of these countries becoming crucial Fintech Hubs in the near future.

Asia, no doubt has become the largest hub for B2B and B2C Fintech solutions hub of the world and holds some of the largest Fintech companies like Ant Financial (US$60Bn), Lufax (US$18.5Bn), JD Finance (US$7Bn) and Qufenqi (US$5.9Bn).

Incidentally, all the four unicorns are from the People’s Republic of China (PRC). There are obvious reasons behind Asia leading the Fintech race and the following Fintech Industry trends in the last few years suggest that Asia will see more movement in the Fintech space.

Why Asia leading the Fintech race?

- Unbanked Populations

Achieving Universal Financial Access by 2020

Credit: World BankIt is said that 73% of the unbanked population of the world is in 25 countries, majorly in Asia. Since more than half of the world’s population is in Asia, Fintech firms have exploited the emerging needs or demands of the mass and have delivered innovative products and services like- Virtual wallets, Internet lending, e-commerce, P2P lending, payment gateways or mPOS. To match the pace of Fintech firms, traditional banks started adopting similar products and services and ended up in digitalization of banks.

- VC-Funding

The Pulse of FinTech Q2’17 Global Statistics for fintech companies

Source: kpmg.com")

Financing for VC-backed Fintech companies in Asia (2012 – Q3 2017)

One of the major reasons for the Fintech industry of Asia experiencing an explosive growth and innovative products and services is strong Venture Capital funding.

‘Ambitious investors are turning their attention to opportunities in Asian emerging markets. It’s Asia, with its enticing mix of booming middle-class populations and rocketing Smartphone adoption, that arguably offers the greatest opportunity for returns on FinTech investments’, according to Michael Lints, venture partner at Singapore-based VC Golden Gate Ventures.

In China, the gradual shift away from a manufacturing-centric economy towards a service and consumer-led economy, coupled with the support of the government through financial incentives, is helping in fostering the innovation and entrepreneurship in the region, which bodes well for the future of VCs.

With the power of the internet increasingly breaking down geographic barriers, and the combination of high speed of internet, higher spending power and a freer adoption of technology means that fintech has an entire market of willing and able customers. Not only Asian countries are presenting opportunities for VC investment but also seen is the greater interest in companies that have businesses that are integrated with these regions, as they can tap into the abundant resources, as well as the enhanced logistics network that has been built over the years.

Furthermore, in an era of decreasing interest rates, investors are considering alternative investment options, making VC funds an attractive choice.

VCs are focusing on unbanked and underbanked sector of Indonesia, with its massive population becoming tech savvy and gaining increasing levels of disposable income. It is the world’s fourth most-populous nation, with Jakarta alone home to 10 million people. The World Bank reported the country’s GDP per capita to have exploded from just $560 in 2000 to $3,374 in 2015, while the Indonesian FinTech Association says fewer than 36% of adults have formal bank accounts.

Not only B2B but also the massive B2C market open ups the lucrative era for VCs. According to Michael Lints, venture partner at Singapore-based VC Golden Gate Ventures, payments is a major area of focus for business in the region.

“A large number of startups are focusing on the B2C payments market because that’s where there is an open gap, especially when you look at the number of people that never use a bank for their payments. For them is has always been cash but now they are using smart phones. Making these devices a means of doing online payments is a big market.

The potential for companies aiming to provide basic financial services in these regions, amid low formal banking usage and rising Smartphone penetration, is massive. Mobile payments, remittances and lending are just some of the very basic services startups are introducing to people for the first time – but other, relationship-based services such as insurance and wealth management are also entering the region.” – Lints”

Fintech investment trends of the past till Q3 2017 show that it already crossed the mark of $5bn with just 203 deals, as against $6.3bn in 213 deals for the year 2016 with VC firms playing a vital role in building a strong startup ecosystem across industries and segments.

The reasons behind VC concentration in Asian Zone are:-

- Southeast Asia has witnessed ascend and proliferation of multiple start-ups, like- GO-JEK, Grab, and KFit.

- Tech-companies had raised $6.5Bn in equity funding by September 2017.

- Grab was able to draw funding of $2Bn from SoftBank and Didi Chuxing.

- Japan’s East Ventures has dedicated $30Mn fund to start-ups in Indonesia.

Various technological adoptions in Asian economics is one of the reasons VCs are attracted and putting money in Asian Fintech Zone. Technologies like AI, Machine Learning, Blockchain, and IoT have a full spectrum of potential use-cases in Fintech industry of Asia. Also, the expected ROI on Fintech Investments are highest in Asia.

The expected ROI in various continents are as under:

Asia- 25%

North America- 23%

Europe- 14%

Global- 20%

“Asia maintained a strong investment pace” in the third quarter of 2017, with 77 completed deals worth $1.4 billion, reported by BRINK ASIA

How is Fintech Shaping Financial Services?

Doing your best is more critical than being the best, and that explains why Asia is the largest and most emerging market for Fintech. It is merely not the innovation happening there, but a significant reason behind upheaval is the ability to transform and embrace the innovation. Asian countries like China and India are fast adapting and adopting the Fintech innovation and has a financial foresight which is much reliable than the west.

The following are the ways by which Fintech has and will shape the financial services in Asia.

The customer demands in Asia and the need of the underserved were understood and served. In China, where the high demands for business and personal borrowing, which remained unmet by the traditional state-owned banking system, were met by the internet and technology platforms. China’s internet giants like- Tencent and Alibaba were the first to introduce Third-Party Mobile Payments and as a result, they had 90% market share of Q1’16’s mobile payments in China.

One of the strong reasons behind Asia’s dominance in the Fintech B2C solutions and investment market is its ability to adapt faster than the rest of the globe. The P2P transaction volume of $5bn was crossed by PRC in just two years whereas the same took four years in the US.

Similarly, B2C Fintech solution of UPI (Unified Payments Interface) and interoperability (allowing transactions across banks) in the Indian market during the demonetization drive in 2016 is strong evidence that Fintech has resolved situations and has provided answers to needs. The non-availability of cash did not hinder the financial transactions for the Indian population and they took the digital transaction mode with a swiftness which witnessed a 400-1000% increase in the transactions.

During the demonetization period (Nov’16- Jan’18) and even after, the value and volume of transactions suggest that Fintech did help. Transactions worth Rs.149.5tn were conducted through digital modes like debit/credit cards. Likewise, the use of debit/credit cards rose by 6.29% in March 2017 from February 2017 and was recorded at 225.7 million transactions.

Fintech sector and its services have made Asian governments recognize the unfolding opportunities in architecting investor-friendly policies for fintech companies. Their support in the mobile payment technology, alternative lending, and Artificial Intelligence driven solutions are a few examples of how the policymakers have realized the need to support the Fintech firms.

Shaping up the future

The following Fintech trends will show you how regulators are shaping the sector for superior financial services and ultimate customer experience:

- Malaysian, Hong Kong, Singaporean governments launched “Regulatory Sandboxes” in the last few years to support…..

- Fintech innovations,

- Facilitate flexible implementation of regulations,

- Safeguard consumer interests,

- Support the development of Fintech Hubs,

- Allow exploration of Fintech B2B and B2C solutions in the controlled ecosystem.

The same will let the regulators understand the impact of the solutions on the society before adoption and will let them take appropriate actions.

- Monetary Authority of Singapore and National Research Foundation established a dedicated Fintech office to strengthen the infrastructure of Singapore Fintech industry and project it as the world’s best Fintech Hub.

On similar lines, Hong Kong Monetary Authority established Fintech Facilitation office in 2016. - Indian government’s introduction of UPI has changed the Fintech markets which resulted in a transformation of mobile payments in the country. The government’s focus on regulations on payment banks and financial inclusion has attracted the largest investment in India in the year 2017.

The cumulative funding in the sector in 2017 stands at US$2.5bn with the following breakup:

Wallet: Paytm raised USD 2.16bn

mPOS: Ezetap raised USD 35bn

Money Transfer: Chillr raised USD 7.5mn

Payment Technologies: Juspay raised USD 5.8mn

Finale

Asia holding the highest number of unbanked population in the world will welcome microfinance in the coming years. Factors like the following will determine the fate of fintech solutions in Asia :

– High mobile penetration in Asia,

– Technology firms holding huge transaction data,

– Difficult to access banks,

– Remittance and money transfer in banks in case of small amounts being less cost-effective, and

– Financial institutions carrying the legacy of low focus on small businesses

These factors will surely provide Fintech firms to further strengthen their platforms in Asian markets which will, in turn, make Asian Fintech market stand unrivaled in all parameters and smile all the way through which they have been aspiring for.

References:

- https://thefintechtimes.com/wp-content/uploads/2017/05/Edition12-final.pdf

- https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/07/pulse-of-fintech-q2-2017.pdf

- https://paganresearch.io/worlds-top-fintech-startups-in-2017-china-rules/

- https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/07/pulse-of-fintech-q2-2017.pdf

- https://thefintechtimes.com/wp-content/uploads/2017/05/Edition12-final.pdf

- https://www.tolamobile.com/

- https://www.pwc.com/sg/en/publications/assets/fintech-startupbootcamp-state-of-fintech-2017.pdf

- https://thefinanser.com/2017/04/whats-like-unbanked.html/

- https://www.ccn.com/asian-fintech-startups-see-record-5-4-billion-vc-funding-2016-driven-china/

- https://www.fungglobalretailtech.com/research/deep-dive-mobile-payments-china/