Teknospire’s Popular Blogs In 2018

We had an amazing 2018, our blogs have been well received by our readers. Here’s the tour of our most loved ones

We had an amazing 2018, our blogs have been well received by our readers. Here’s the tour of our most loved ones

When was the last time you stepped into a brick and mortar bank branch for financial transactions? It sure has become a rarity for many of us, maybe even unheard of for most millennials. Most banking operations are just a click away today. Welcome to Digital Banking! As advanced as it may seem now, banking has been among the oldest professions in the world. Did you know that some banking operations took place as early as 2000 B.C? Facts aside, at present, the winds of technological change are sweeping over the mammoth banking industry not just as digital banking in Europe but even in the remotest corners of the world. It’s an exciting time for emerging innovative banks and financial institutions, while the big banks have no choice but to get a makeover into a new digital avatar. History of Banking Europe was at the center of banking activity even in its earliest crude form. The word ‘bank’ comes from the French word ‘banque’, the Italian word ‘banco’, and the German word ‘banc’ which means a bench or a counter. Lenders would typically set up desks inside huge building structures or a market square. Italy was the hotbed for international trade and banking transactions. The Italian cities of Florence and Venice saw early banking activity with transactions through checks and bills of exchange as we know them today. The first bank was established in Venice in 1157 backed by the state. As civilization entered the 20th century, banks evolved and became more sophisticated. Adoption of Digital Channel in Europe More recently, the roots of digital banking in Europe can be traced to the advent of ATM machines in 1950s-1960s. The humble cash-whirring ATM machine and its computer infrastructure turned out to be a game-changer in the present-day banking ecosystem. With the ushering of the internet during the 1990s, banking got propelled to a different stratosphere. By 2000, the world was at our fingertips as every handheld mobile phone. Scandinavian countries and Europe welcomed the internet and digital banking as they enjoy one of the highest rates of internet penetration even today. The huge user base in Europe has made it a natural breeding ground for FinTech companies who hold an edge over banks in software technical know-how. Some of them started inching into the banking space, sometimes without a banking license while some others in partnership with existing banks. Such firms came to be known as neo banks. They had the platform and offered banking products as a savings account and a credit card to customers. Also emerged are the challenger banks, those with a full banking license. However, it is not merely the internet penetration that has made FinTech companies a force to reckon with. A Deloitte study shows increasing demands from customers for a better digital experience along with competitive pressure has resulted in digital banking champions. Adapting to Digital Banking – Initiatives by FinTech Firms and Banks The global financial crisis in 2007 wiped out the trust that people had in big financial institutions. Neo banks in Europe and challenger banks cashed in on this mistrust by offering a refurbished banking experience to the common folk. Right from an innovative product line-up, more transparency, user-friendly facets, and a snazzier look, digital banks have managed to win people’s trust in Europe with their digital banking initiatives. While the grand old banks focused on regaining their assets after the crisis, the much smaller challenger banks have tapped into the largely ignored retail consumer base. It took Berlin-based N26 less than a year to get to a million users when it started out in 2013. Similarly FinTech start-up Revolut has two million customers as of today. These intuitions have depended largely on their innovation and ingenuity to rope in customers and remain visible even among the big banking names. Use Cases of Digital Banking In Europe Fidor: Munich-based Fidor group has been one of the torch-bearers when it comes to FinTech innovation. In 2017, it launched its own digital community-based marketplace for financial services ‘Fidor Finance Bay’ in partnership with US-based experience design studio: ‘Eight Inc’. Thus, unlike the cut-throat competition among banks, FinTech companies have turned aggregators, leading to a buzzing marketplace. Holvi: Another case in point is the Helsinki-based ‘Holvi’ that started with offering a current account and a debit card to customers. It partnered with a German Mobile Point of Sale provider ‘SumUp’ to lend to SMEs and retail clients for a headway into the country. What’s interesting is that at a time when companies are still struggling with the transition on to cloud platforms, Holvi’s software infrastructure is already hosted on a cloud with Amazon Web Services (AWS). Monzo: Four-year-old bank Monzo has taken banking to the next level. With no branches, customers can interact with this bank only through their mobile phones, helping the company cut some costs. A user-friendly app for a personal finance-distraught millennial generation has managed to widen its heir client base rapidly. N26: N26 already operates in 17 countries and plans to start operations in the US very soon. What’s unique about some of these companies is that they have used a particular component of banking services to build their operations and get a banking license thereafter. Be it hosting their database on cloud platforms or using third-party solutions on a front like the four-year-old London-based Starling Bank, or using Application Program Interface such as TrueLayer that provides updated account information and payment initiation services. The impressive technological infrastructure hosted by FinTech companies and Challenger banks makes it a natural engine for growth. The big banks that have embraced innovation in the banking sector have been rewarded. DBS Bank was named as the world’s best bank in 2018 by ‘Global Finance’ for its leadership in digital transformation. Euromoney has also conferred the Singapore-based bank as the best digital bank in 2018. Digital Banking OPPORTUNITIES in Europe Artificial Intelligence and Machine Learning Artificial Intelligence and Machine Learning could be the next biggest

“Financial Institutions must be able to deliver and easy to navigate, a seamless digital platform that goes beyond a miniaturized online banking platform.” -Jim Marous, Publisher – Digital Banking Report How many of you have actually visited a bank in recent times? Do you remember the last time you visited a bank to transact money? Not sure, right? The reason for this can be understood better if you acknowledge the fact that you live in an era of digital banking. Your buying behavior and modes of payment have changed drastically over the last decade. Cheque and cash are old schools now, and it is more about online banking, mobile banking, and Internet banking. This cashless economy has not only made things easier for you but has also made it all instant and quick. You no longer have to carry wads of cash or wait for banking hours to receive and transact money. While you do have quite an options when it comes to virtual banking, here, we would focus majorly on digital banking, mobile banking, open banking, and online banking. So here is the primer on different ways to bank. Online Banking You are using online banking service every time you log in to your online bank account. In other words, transactions conducted electronically using the internet as a gateway are called online banking. “Online banking refers to banking services where depositors can manage more aspects of their accounts over the Internet, rather than visiting a branch or using the telephone. Online banking typically is comprised of a secure connection to banking information through the depositor’s home computer or another device.” – Techopedia Pros of Online Banking Almost every financial institution nowadays gives this facility to its customer to reduce the hassle of visiting their physical branch. Some banks even allow you to deposit cheque by simply taking a picture of it. No more tedious process of banking with the long queue with restricted working hours and unpredictable weather conditions with equally unpredictable mood swings in hot, sweaty and humid conditions. With the advent of online banking, a person can virtually monitor and transact money 24/7 without having to wait for the banking hours. Also, the alert messages and emails allow you tomonitor your account anytime and detect any fraudulence well in advance. Cons of Online Banking The biggest drawback of this mode of banking is that it can’t be used to deposit and withdraw money. Also, your online banking experience is dependent on your internet connectivity. Digital Banking While there is a tendency among people to confuse this term with online banking, digital banking is definitely not the same as the former. While online banking literally limits you to the services provided by your banks like NEFT transfers, automatic payment reminders, and the likes, digital banking goes beyond this. Online banking focuses on digitizing the “core” aspects of banking, but digital banking encompasses digitizing every program and activity undertaken by financial institutions and their customers. Pros of Digital Banking When you talk about digital transactions, you think of mobility, feature-laden transactions, predictive and profile-oriented banking with functions like booking tickets online and purchasing a product/service online. It is also about using e-commerce businesses for doing your day-to-day transactions and your regular online banking without any hassle on-the-go. Digital banking also means attractive cash-backs, discounts, and vouchers while transacting digitally. Cons of Digital Banking While the advantages outweigh the disadvantages, there are a few drawbacks involved in digital banking as well. You may not be very comfortable making large payments digitally. Also, you may tend to get lured into unnecessary online shopping just to use the cash back and vouchers that you get whiletransacting digitally. But who considers shopping a drawback ever, right? Internet Banking You may say that online banking and internet banking are the same. Yes, agreed! However, there is a new facet of online banking that goes over and beyond the understanding and scope of online banking. Open Banking! Ever wonder what that means to you? Through this concept, people can share their transaction data with third parties to boost competition in the financial market. Sounds interesting, right? Pros of Internet Banking It allows you to initiate and make payments directly from your account as a bank transfer. It also enable you to keep a check on your finances in a better way. Through open banking, you are not only transacting, but you are also streamlining your finances andmanaging it more effectively. With this, you can also get more customized services as per your spending behavior, leading to a more responsible and systematic lending process. Cons of Internet Banking This concept is relatively new, and that literally translates to many trial-and-error instances and a general mistrust related to its security and authenticity. People who are not adept at digital technology might not be able to reap its full benefits. Mobile Banking You all have used this at some time or the other. Every financial transaction you undertake using your Smartphone applications is termed as mobile banking. Apart from the commercial apps, your financial service provider would also have a mobile app with which you can transfer cash and make bill payments conveniently on your mobile. This is by far the most trending among all the banking types, and the onus is that you would only need your Smartphone and an internet connection for this kind of banking! Pros of Mobile Banking Mobile banking has a lot of scope in the virtual banking space and encompasses transactions through mobile wallets, digital payment modes, UPI transfers (like the BHIM app), etc. There are many mobile apps which offer you safe and secure transactions and much more, ‘anywhere – anytime’ with just a click. For example, SBI has SBI Yono, SBI Anywhere; ICICI Bank has iMobile. HDFC has HDFC Mobile and Pay Zapp. Kotak Mahindra’s Banking app is Kotak 811, while Axis Mobile provides Axis Mobile. We also have Payment Banks committed to the inclusion and service to the last

Digital Banking is all about the transformation, where the consumer rather than the technology, is in the driver’s seat, and this MATTERS. It’s about digital money deposits, withdrawals and transfer of money from one account to another. It’s also about Account Management to loan management to paying all your bills digitally. Digital Banking essentially entails the leveraging of technology, where banking services are delivered over the internet, by involving high levels of process automation and web-based services. What Is Digital Banking? Digital banking, in simple words, is emulating 90% of the services provided by a conventional bank branch digitally, via a mobile app or through net banking in your computer browser. Welcome ‘Digital Banking’. Welcome to the virtual world of banking services! Channels of Digital Banking Just as the word “virtual” is put up, you might wonder about the channels existent to avail such services. Let’s take a look at a few. Today, the main channels of digital banking are the Android and iOS apps of the respective banks and their browser-based websites. These apps are easily available in different app stores like Amazon Appstore, SlideME, Samsung Galaxy Apps, Mobile9 and so on. For example, SBI has SBI Yono, SBI Anywhere; ICICI Bank has iMobile. HDFC has HDFC Mobile and Pay Zapp. Kotak Mahindra’s Banking app is Kotak 811, while Axis Mobile provides Axis Mobile. We also have Payment Banks committed to the inclusion and service to the last mile like PayTM, Vodafone m Pesa, Airtel, Fino, Indian Post, Jio and so on. Babies on the block: Neo banks & Challenger banks In this race, we are also joined by Neo banks and Challenger banks (Read ‘Tomorrow’s Bank’) like Revolut, N26, Monzo, Atom, Yolt, WeBank, Moven, Fidor, and MYBank to name a few. These banks are an important part of the emerging cohort of FinTechs which puts customers at the center of everything. They are the banks which are reinventing the practices and processes associated with the traditional banking. A new type of digital bank (often working solely through a mobile app) which exists without branches. These are 100% digital banks. Neo banks don’t have the license and they rely on a partner bank to operate. On the other hand, Challenger banks have the full banking license and offer full suite of banking products. They compete independently and on equal terms with traditional banks or digitally manifested traditional banks. They offer: Reduced costs Advanced features User friendly interfaces Customized reports Fast account openings ( between 3 to 10 minutes) International ‘Multi Currency’ Payments Instant ‘Multi Currency’ Payments 24/7 support Vaults and Expenses Analytics All these to ensure simple, secured and seamless transactions! Digital Banking Features Listing some of its many features: You can apply online for opening a savings or current account from your desktop or mobile. A manual call from a bank representative follows, who then completes verification from a remote branch. OTP, video authentication and upload of scanned documents are proceeded with. This enables low cost zero balance account. 24/7 query solutions by chatbots are available in your app or net banking facility. Provides a highly secured, encrypted money transfer. Enables 24/7 money transfers at minimum or no extra fees, and displays their records whenever necessary. Electronic payment of bills to the pre-registered payees. Offering customized pre-approved all-purpose loans to the customer via a digital channel. Advantages of Banking Digitally Some of its many advantages will surely help you in forming a fair view of digital banking and its multi-faceted applications: Visiting a branch and spending precious work time is eliminated. Paying your bills online, keeping track of your transactions and tab on your spending has become easier. Customized approval for a loan via Artificial Intelligence using CIBIL in minutes for a customer. Avail discounts on your favorite activities right there from your banking app. Digital Banking provides with a virtual debit card, whenever you wish to generate one. Without a permanent CVV and duration of 24-48 hours, these are much safer. Real-time interbank payment is now the norm through IMPS while BHIM (Bharat Interface for Money) and UPI (United Payment Interface) enhance the interbank payment security. Multiple money applications can be synced together. Online budgeting was never so easy. Real-time figures, anytime, anywhere. Multiple sources of revenue for the bank. Cost of providing digital banking services is a fraction of branch bank services. Cons of Digital Banking Like any other novelty, digital banking also comes with its own set of disadvantages: Not possible without a stable internet connection. With scraping of Aadhaar for authentication, the model of digital verification that’s the cornerstone of digital banks is at risk. Chatbots and Robo advisors are not always the best option for the query. Unless they have the algorithm to learn from new questions, sometimes they loop back to the same answer for different queries. When products like FD, which are linked to the performance assessment of a bank employee, are done online, no particular back employee gets its credit. This leads to disinterest in that product in the bank employees of that branch where it’s registered. Few Dos and Don’ts in Digital Banking (Source: TribuneIndia.com) While banks and FinTechs take all precautions to ensure security, it’s always advisable to know the dos and don’ts of digital and online banking. Here are some of them: Always keep them password protected. Change your passwords and security settings regularly. Always visit your bank’s secure Internet Banking site directly. Always verify your domain name. Log out of your Internet Banking account the minute you complete transactions. Use dedicated/secured WI-FI networks only. Always use, and update Antivirus software to keep your information safe. Safety tips while using a mobile app for banking transactions: Never save your mobile banking log-in and password on the phone. Never leave your handset unattended. Always lock your phone to prevent unauthorized use. Notify your bank as soon as your mobile is lost or stolen. Update the apps regularly. Keep an eye on your account balance and transaction history regularly. How FinTech

Financial Inclusion helps lift people out of poverty and can help speed economic development. It can draw more women into the mainstream of economic activity, harnessing their contributions to society. – Sri Mulyani Indrawati, Indonesian economist, Minister of Finance of Indonesia since 2016 Economic growth of a country depends on factors like national income, per capita income & per capita consumption, technological advancement and even its political structure. An equilibrium between savings and consumptions is another factor which decides economic growth. Walter Bagehot, the famous classical economist, stated long ago that a strong financial system is crucial for economic growth and that the lending should be “quickly, freely and readily”. Translated to suit modern day scenario, to strengthen financial systems you need to encourage economic activities like Financial Inclusion, Digital Banking & Fintech. Let’s explore what and how Financial Inclusion can do and what it holds in the future for developing countries like India, Nepal, Bangladesh, and other African and Asian economies. Defining Financial Inclusion Financial inclusion can be broadly defined as the process of making financial services available to people, especially the weaker sections and low-income groups of the society. It includes the timely and adequate availability of a wide range of financial products and services like: Bank accounts for saving & transactional purpose Equity products Insurance Saving products Loans For economic growth in developing countries, this aim is furthermore towards ensuring financial inclusion to the unbanked and the underprivileged community who are either unaware of or unable to affordable financial services and products. Penetration of financial services to all sections of society at a swift pace can be achieved through Digital Banking and FinTech. Goals to achieve Financial Inclusion are: To maximize the use of the latest technologies to transform the existing traditional financial or banking service models. To better the existing products or services of the financial sector. Financial Inclusion – Impacting Economies of Developing Countries Impact of Financial Inclusion, especially via Digital Banking or FinTech, can be exponential. A survey report by McKinsey Global Institute, which has been endorsed by the World Economic Forum also, states that there are more than 2 billion individuals and 200 million businesses (small, medium and micro) with no formal access to financial services like savings or credit. Those who have access are often required to pay heavy fees or charges. It goes on to state that if through Digital Banking, financial inclusion is ensured then the following impacts are expected: GDPs of developing countries like, India, Ethiopia, Nigeria, and similar Asian economies will increase by 6%. The absolute value of such increase may reach a whopping $3.7trillion by 2025. This incremental GDP thus created will generate an additional 95 million new jobs across industries. Addition of 1.6 billion unbanked individuals will create a big pool of loan borrowers. Around $2.1 trillion of the loan amount to these individuals or small sized businesses is expected. Governments can bring down tax collection leakages and gain up to $110 billion per year. Governments stand to gain up to $400billion every year when they convert traditional accounts to digital accounts as they can now save 80-90% of cost on managing traditional accounts. Increase in customer base will result in an incremental revenue generation of $4.2 trillion. All these predictions sound exciting, right? Read on to know some of the many concrete benefits of financial inclusion. Concrete Benefits of Financial Inclusion The few of the many, main benefits of financial inclusion are: Better Penetration of Services With financial inclusion in place, reaching the rural populace will be made possible providing them easy access to bank accounts, cash payments, cash receipts, and account statements. The authentication and fulfillment of services can be done by fingerprint and online receipts respectively. Boosting Economic Growth The banking ecosystem will be strengthened as the cash economy will be reduced and the habit of saving will be inculcated in rural masses. Direct Subsidy Transfer The government subsidies will be directly deposited to the bank accounts of beneficiaries. The funds will thus reach the intended recipients instead of middlemen forestalling leakages and corruption. Encourages Entrepreneurship Financial inclusion will motivate formal banking and transparent credit availability which will release people from the clutches of unofficial money lenders. Adequate credit will prompt entrepreneur initiatives which will further enhance economic outputs and prosperity of the country. Financial Inclusion – Headway The progress of financial inclusion in the context of emerging economies like India has been substantial. The same has been highlighted in the Department of Financial Services GOI reports as: 35.5% of households availed banking services in 2001 which grew to 58.7% in 2011. This growth is significant in rural India –from 30.1% in 2001 to 54.4% in 2011. The CRISIL- Inclusix which includes branch penetration, deposit penetration, and credit penetration was 35.4 in 2009 and has grown to 40.1 in 2011 to 58.0 in 2016. IMF ‘Financial Access Survey 2018’ reported the following- Low-income countries like- Bangladesh, Myanmar, Guyana and many African countries have successfully used mobile payments for Financial Inclusion. These countries have more than twice the number of bank accounts per 1000 adults than the developed economies. What a sky-high improvement! Additionally, the IMF Financial Access Survey 2018 also reported an increase in the number of ATMs per 100,000 adults, branches of commercial banks per 100,000 adults, deposit and loan accounts with commercial banks per 1000 adults. Mobile money transactions number per 1000 adults was the most attention-gainer with a significant rise! Financial Inclusion does not mean only access to services but how those services are useful for the user. One of the parameters which are considered by various organizations while mapping FI is the safety and convenience of the financial service or product. A survey done by the World Bank Group, measuring the Financial Inclusion and Fintech revolution, reported that globally the percentage of adults using digital payments for receiving and making payments increased by 11% between 2014-2017. In developing countries, it is higher by 1% i.e. 12%.

Banking, as a domain, has always been a competitive one. To keep up with the pace of the dynamic nature of this sector, banks & financial institutions are gradually making the shift to experiment with newer technologies, like Open Banking and innovative concepts like FinTech, designed specifically for the banking sector. The basic idea behind all these innovations remain to offer a better experience to consumers and leverage the choice of integrated systems that are widely available today. Are you OPEN to Open Banking? The impact of technology in making our lives better and smoother can’t be overemphasized enough. FinTech (an excellent combination of finance and technology!) is one such area making the traditional banking system seem redundant with each passing day. The rise of Fintech sector has been exponential in the last few years with Fintech adoption seeing a sharp rise globally from 16% in 2015 to 33% in 2017 on an average. Open Banking API (Exclusively covered as Open Banking API: A Journey, 1st part of this series of 3) is the newest offering of FinTech that holds immense potential to bring about a transformational banking experience to its end users. However, before making the switch to Open Banking, it is essential to understand what the concept is trying to achieve and who will it really benefit? So What’s the Buzz called ‘Open Banking’ All About? With Open Banking, banks are moving to Agile technologies, building strong partner networks, and creating robust mobile platforms which cater to consumer’s needs, thus enabling direct financial transactions between customers and businesses and making cross-platform payments a reality. It works as a systematically designed collaborative model. Here the customer’s banking and other financial information/data is shared to trusted third parties (with the customers’ consent, of course!) through APIs with the aim of offering enhanced capabilities to the users. Thus, Open Banking is a financial services term as part of the financial technology that refers to: The use of Open APIs that enable third-party developers to build applications and services around the financial institution. Greater financial transparency options for account holders ranging from Open Data to private data. The use of Open Source technology to achieve the above. In short, “Open Banking is the possibility of creating new digital business and ecosystems through APIs provided by the banks. This allows customers: To have a greater control over their data Have a better experience in a secure, agile, and future-proof method To generate new revenue streams, and to create a long-term sustainable service model for the industry as a whole. Who will ‘Open Banking’ Really Benefit? The benefits of an Open Banking model aren’t just limited to consumers but extend to service providers as well. It benefits, one and all, associated with it. Benefitting Consumers Among the many benefits of Open Banking to consumers, the most important include:Giving the Benefit of Choice to Customers As a service provider, banks generally offer limited options and the same services to all their customers. Open banking, on the other hand, gives the benefit of choice to customers as they now have the freedom to select from multiple service providers available. It also empowers customers to take charge of their finances and make informed decisions to manage their accounts. Easing Payments with Smart Devices With Open Banking APIs, customers won’t have to wait in long queues to make purchases using physical wallets at stores. The concept will allow emerging technology applications such as Google Pay, Samsung Pay, Apple Pay, PayTM etc. to make payments using digital wallets using your Smartphone or smartwatch. Ease of Remittance and Currency Exchange Increased number of migrants across the globe for better economic opportunities means an increased amount of money to be sent back to their families. Banks have always found international money transfer and remittances to be a painful and expensive process.Instead of paying a large transfer fee to the ‘money transfer businesses’ or facing the lack of proper setup, especially in rural areas, FinTech companies like NDASENDA, have made this entire process extremely simple, smooth, less expensive, and much faster. Thanks to Open API, the money can be transferred, services can be bought and bills can be paid seamlessly by using one single mobile App at the comfort of your home. Various service providers such as We Swap, World Remit, mPesa etc. are offering ‘currency exchange services’, by using Open Banking, in a very secure and seamless way to transfer even minuscule amounts of money overseas. Customized Product Offerings Open banking holds the potential to offer customized and relevant product & service options to the consumers which most banking apps fail to do. Open banking APIs introduce the concept of service personalization in banking to benefit customers immensely. Customers can now have access to multiple accounts in one place. The customers will be able to enjoy the best deals available with greater transparency. An opportunity is here to see your current financial position in a single application on your Smartphone. It is just a matter of ‘single click’. All the financial data at one place gives the consumer the leverage to take quick credit decisions and avail the best deals possible. Open to better offers by credit providers and instant credit and remittance of the same. With all the accounts linked together by an app and available on a single platform, the consumer is ‘all-powerful’ to make a choice in how to pay. This will also bring in some innovative offers by the banks and the financial institutions to make new customers and retain the old ones. It’s raining Profits! Benefitting Banks and Financial Institutions Collaborative Advantage Open Banking gives an opportunity for banks to stay ahead of the competition by letting them explore data-sharing agreements with fintech and other non-financial service institutions. Allows Banks to Be Futuristic The model allows banks to be futuristic by letting them understand both data privacy mandates that exist as well as the likely changes they need to adapt for a better customer experience. Thus making decision-making foresighted and insightful.

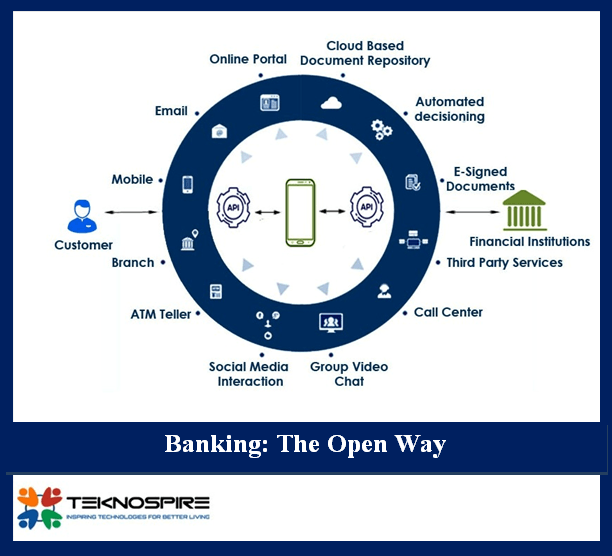

Data sharing and Big Data have become the trending topics in the financial world of late. With the advent of many Fintech start-ups, traditional banks are undergoing a major shift. They, now, are looking forward to modifying the way they operate, to survive the cut-throat competition from their peers. This is when the idea of Open Banking started doing rounds in the banking arena. What Is Open Banking API? In short, it is an Outbound Trade – Stretching beyond the 4 walls of the bank for better services to the customers. The concept relies on connecting computing systems through a common digital language shared among them with the aid of an Application Program Interface (API). Open Banking is a financial services term as part of the financial technology that refers to: The use of Open APIs that enable third-party developers to build applications and services around the financial institution. Greater financial transparency options for account holders ranging from Open Data to private data. The use of open source technology to achieve the above. Thus, “Open Banking is the possibility of creating new digital business and ecosystems through APIs provided by the banks.” This would increase the level of transparency with respect to data accessibility for end customers. It would also help Fintech firms and other third parties to develop and build financial applications. This, in turn, would help banks and other financial institutions to look beyond their businesses and make innovatory advancement in services for the end users. How Did ‘Open Banking’ Concept Take Flight? Open banking was developed based on an idea of Open Innovation coined by Henry Chesbrough who was the head of Open Innovation, Haas School of Business. He came up with the idea that an information or knowledge doesn’t belong to a singular entity and needs to be shared. This concept was later taken up by the banking sector as ‘Open Banking’ to innovate the way they operate and give a holistic banking experience to its customers. Data Sharing – The Journey so Far Until recent times, your financial history was closely guarded and protected by your bank. Your data could only be accessed when you use your debit or credit card for certain transactions through the payment processors. Hence unless you are officially validated, you can’t access an individual’s banking history. However, your banking data still found a way to get to other companies who could use it for their business promotion. How was that even possible, you may ask! Screen Scraping The only way one could get hold of your financial history was through screen scraping. This was possible by getting your login credentials and using that to access your account for the required data. This was not only unsafe and risky but also highly inconvenient as it gives the said company access to your most confidential information (that could also be misused) and might even lead to frequent blocking of your account (in case of suspicious activity). Hence this needed fixing! The most important part here is the need to control the data that you are willing to share and also the power to revoke it whenever you feel the need to. Open Banking API to the Rescue! To give a control over their data to the customers, banking institutions adopted a newer and updated technology which shared the banking data between the third parties through APIs. This is a sustainable model which is not only reliable but also secure. However, on the flip-side, such advancements may lead to conflicts and need strict governance and policies to control the technicalities associated with such an arrangement. Also, such data sharing systems need high-grade security controls and infrastructural barriers to contain the data privacy. The All-New PSD2 Standards for Data Security! The revised Payment Services Directive or the PSD2 is an upgrade of the existing directive to regulate and control the payment services and service providers in the EU. The main aim for this revision was to minimize conflicts between two or more third parties involved in data sharing and to ensure consumer protection and data privacy. In fact ‘PSD2 + Open Banking and APIs’ is considered as an Engine for Innovation and meaningful change. This directive is said to be of monumental importance in the legacy of data sharing in the retail banking sector. It would control the way the APIs behave and are controlled. They would dictate how third parties connect, share information and the scope of information that can be accessed. By this, the Third Party Providers (TPPs) registered across the participating states can communicate with any bank provided they clear the SCA (Strong Customer Authentication) norms and the data exchange also conforms with the SCA norms. This would mean that every third party involved in data sharing would have to go through diligent scrutiny to verify their authenticity. Open Banking: Inbound trade @ Teknospire Well, it’s not only about the Outbound Trade, Open Banking is also about Inbound Trade. It is also about trading the right products and service features seamlessly from Third Party Partners (TPPs) into their own offerings. Importing the full breadth of these products and features enhances personalized customer experience, build customer loyalty and it also lowers bank’s operational costs. With Open Banking, by adding ‘Banking and Non-Banking’ products and features, banks are able to extend their services beyond the ‘traditional zone’ and broaden their approach beyond financial services to complement further as ‘Complete Customer Banking Journey’. Teknospire, a FinTech Company, has helped multiple banks and financial institutions in multiple countries in Africa (Zimbabwe, Mozambique, Zambia, South-Africa), India, Nepal, and Bangladesh. The core mission and vision are to serve the Bottom 2 billion population, who are not on the digital payments platforms yet. Teknospire enables the banks / financial institutions to build a digital ecosystem with Omni channels interface, along with all possible digital services dispensation at the last mile. The services can be disbursed via B2C interfaces or through the assisted channels (digital touch points/agent network). To be able to digitally evolve the banks

Creating a strong business and building a better world are not conflicting goals – they are both essential ingredients for long-term success”. – William Clay Ford Jr., Executive Chairman, Ford Motor Company. With corporations becoming more responsible towards the society, this concept has evolved into what we today know as Corporate Social Responsibility (CSR). CSR has been increasingly recognized as a means for businesses to serve communities in the best possible manner. It has also made the consumers feel a sense of attachment with the business entity. What is Corporate Social Responsibility? Corporate Social Responsibility can be understood as a business model that is aimed at Corporates to become socially responsible and answerable to its stakeholders and to the public at large. Corporate Social Responsibility, on one hand, has helped businesses with better interaction with consumers and on the other hand, has had stakeholders develop loyalty towards the business. It also has enhanced overall reputation – a powerful statement of what they stand for, in an often cynical business world. Jason Potts, a senior associate with the International Institute for Sustainable Development (IISD), who is taking care of sustainable markets and responsible trade initiative, says: “CSR is fundamentally about ensuring that companies forward broader public objectives as an integral part of their daily activities and this can only be ensured with the appropriate communication channels with stakeholders.” “CSR policies need to be considered as a core and inseparable component of the overall service or product offering”, he further adds. Importance of CSR to Corporates Companies that display their concern towards various social causes are surely better off than those that don’t. CSR has the ability to change dynamics for any given corporate. For Klara Kozlov, head of corporate clients at the Charities Aid Foundation, “CSR allows businesses to demonstrate their values, engage their employees and communicate with the public about how they operate and the choices they make, to ensure a sustainable future. CSR helps pave the way for partnerships between businesses and civil society that are based on common goals and shared actions to deliver impact-driven outcomes.” Few of its benefits include: Public Image Social responsibility not only improves an entity’s public image but also helps it become a consumer-favorite in no time. Enhances Engagement of Employees Companies, which show their interest in improving the society’s well being, attract and retain hardworking as well as valuable employees. Not only this, those hired demonstrate better productivity and strive for better profit margins. Retention of Stakeholders Investment in Corporate Social Responsibility indicates a company’s strong ethics and high standards. Such outlay, in the eyes of investors, prove that the company does not solely care about profits but also has a sense of duty towards citizens. Such a display of sound business policies certainly attracts and retains investors. Reduction in Operational Costs The concept of CSR also helps a business reduce its operational costs to a great extent by opting for business practices that do not affect the public adversely. For instance, by option for green technologies and reducing emissions & waste, companies save a great deal of cost. It can be said that CSR has a dual positive effect on both, the consumers as well as the business. Problems Companies Face with CSR Corporate Social Responsibility has become a complex phenomenon with companies developing holistic policies to address the demands of the public. As such, there come several problems related to the execution of initiatives such as disbursal and tracking of funds, cost-benefit issues, etc. We try to highlight the major problems that companies, the world over, face with respect to CSR. Disbursement of Money Every company indulging in CSR has an exclusive monetary account through which the company disburses money for various causes. However, due to lack of digitization, such money is disbursed in the most haphazard manner, making it practically difficult to keep track of the amount. Accountability of Money: Once disbursed, there is hardly any check on how such grants are being deployed and utilized by those concerned. This makes it almost impossible for an entity to recognize the cost benefit of their contribution. Sans any digitization of money movement, amount once paid out is nowhere to be accounted for, indicating lack of answerability and utter pecuniary wastage. Sustainability of CSR activities: More often than not, the amount spent with huge fanfare falls short of giving estimated returns to the business over time due to lack of diligence and monitoring. Initiatives become difficult to sustain owing to a deficiency in digital regularization. Role of FinTech Companies in CSR Over time, FinTech companies have been recognized as an imperative element of business operations, especially with respect to CSR activities. FinTech companies or simply put, companies designing and developing technological and digital programs to aid financial or banking operations and services help businesses immensely in regulating the financial approach. Employing a FinTech company to CSR activities can contribute greatly to any business. Digital Payments Mobile wallets and app-regulated payment disbursal portals have made the transfer of money as smooth as ever. Corporate entities save on crucial time and money spent on such disbursal while opting for digital methods. Bridging the Gap: The core area of all CSR activity for a majority of companies are the rural and underdeveloped areas where financial exclusion is a major problem. However, FinTech companies are bridging the gap between the lender and borrower and even reaching people who do not own a bank account. They are further helping the customers by providing assistance before, during and after the financial transaction by extending the ecosystem of the banking system. Countries that have a majority of the population thriving in rural areas have finally had access to banking, thanks to the inception of FinTech. For instance, Bangladesh has about 70 % of people living in the rural areas where not even half of them own a bank account. To cover the deficiency, ‘bKash’, a FinTech initiative, allows such people to receive as well as send money through mobile phones. Crowdfunding: FinTech’s

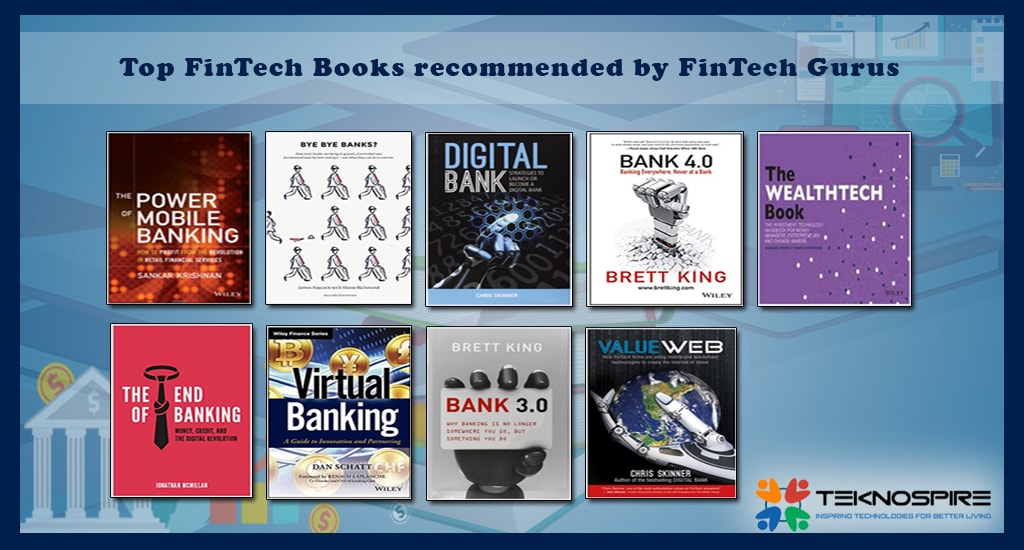

The value of FinTech investments globally in 2008 was 1 billion USD, which rose to 10 billion USD by 2014 and is projected to touch 46 billion USD by 2020. So much is happening around FinTech but how much you know about FinTech is the question. Are you in touch with ‘How the latest development in FinTech can impact your daily routine?’. Strongly recommended by the top shots in the FinTech industry, these FinTech books hold the key to many of your answers. Happy Exploring! Digital Bank To know about innovations happening in banking and how Mobile Banking is transforming the way consumers interact with the banking industry, “Digital Bank” by Chris Skinner is a must-read book.Chris Skinner is one of the most influential people in banking whose works have earned him the sobriquet “Fintech Titan”. He has not only guided the readers in an exhaustive way about the digital revolution but also depicted the way existing banks like Barclays in the UK, start-ups like Metro Bank and disruptive formats like FIDOR Bank, have focused on modern technologies, in redefining the banking sector. Strongly recommended by Seth Wheeler, former Special Assistant to the President for Economic Policy at the White House, City AM and The Financial Brand, it is a must-read for all, be it a professional, a banker or a Fintech enthusiast. Digital Bank signifies the need for digitalization of banks. Chris justifies his status as an independent commentator on the financial markets and Fintech. ValueWeb Chris Skinner has masterfully illustrated the complexity of the Internet of things and Internet of value in his book ‘ValueWeb’. He has thoughtfully used the resolutions which were utilized by Fintech companies to solve the problems faced by the old systems by collaborating “Internet of Things” and “Internet of Value”.Skinner, who chairs the European Networking Forum- The Financial Services club, highlights the convergence of technology, e-commerce, and finance which are being combined by them to build the ValueWeb. Backed by the likes of Seth Wheeler, former Special Assistant to the President for Economic Policy at the White House, business-focused newspaper City AM and The Financial Brand, this book covers how ValueWeb permits machines to trade with machines and people with people across geographical boundaries in real-time with speed, precision and with zero cost. This well-researched book is of great interest to people curious to get a glimpse of the future of FinTech. The Power of Mobile Banking ‘The Power of Mobile Banking’ is a combination of guide and tutorial to banking professionals on how they will face competition from telecoms, E-Commerce retailers, and technology companies.Sankar Krishnan, having more than 25 years of experience in banking and financial services, strongly suggests the traditional bankers that ‘Mobile Banking’ and the ‘Internet of Things’ are the things of today. Banks need to streamline themselves to deliver the populous demands of personalized banking experience via Mobile Banking. In addition to rendering strategies for adapting to Mobile Banking to benefit customer and revenue, he has taken a step further by covering the risks, hazards, and wealth opportunities which lay with Mobile Banking. Recommended by Parameter Insights and Fintech News to name a few, it is a must-read book for bankers and professionals, especially associated with traditional banks. Bank 3.0 A renowned futurist, keynote speaker and four-time bestselling author- Brett King released his first book “Bank 2.0” which was a bestseller on Amazon in the US, UK, Germany, France, and Japan.Followed by this, he wrote “Bank 3.0: Why Banking is no longer somewhere you go, but something you do”. It focuses more on financial services and payments like the widespread use of Mobile Wallet and also talks about the impact of social media on the banking ecosystem. The book illustrates more on the perspective formed by tablet computing to the operational engagement of the cloud. Brett has elaborated on how FinTech has created a community which includes de-banked customers, who don’t need a bank at all. He shows that FinTech companies can leverage the opportunities created by the gap between customers and financial services players. No wonder it got likes and extensive coverage in Fintech News. Bank 4.0 Highly recommended by FinTech News, this masterpiece by Brett King is next in the series after ‘Bank 2.0′ and ‘Bank 3.0′.The best-selling author, in ‘BANK 4.0: Banking Everywhere, Never at a Bank’, envisages what banking might come to look like in the coming decades as he portrays his vision of the future of banking in the next 30-50 years time. He discusses how cash, cards, and the conventional banking ecosystem will be redesigned. Snippets of his vision of what banking will become include a completely transformed banking ecosystem where ‘Selfie-pay’ will work in China, ‘blockchain’ will exist in Africa, and ‘self-driven cars’ will have their own bank accounts. King continued that the best investment advice is coming from algorithms and robo-advisors that can adapt your portfolio in real-time as markets shift. “The banking system of tomorrow is being built from first principles today and most banks won’t survive to see that future banking system.”, claimed King. The WealthTech Book The book gives you an in-depth insight into the digital revolution that has happened over the years. It can be an excellent guide for entrepreneurs, investors, innovators, analysts, and consultants.Authors, Susanne Chishti and Thomas Puschmann have focused on the “Wealth Management Sector” and the impact of technology on it. Susanne Chishti, CEO of ‘Fintech Circle’, founded Europe’s first ‘Angel Network’ focused on Fintech opportunities and Fintech Tours. She and Thomas have successfully guided investors by explaining how investors can achieve better returns on their investments in FinTech. In this book, they have explored how technology and start-ups can influence disruption in order to enhance customer satisfaction. Greatly mentioned by FinTech News, the book contains motivational success stories, business models and exhaustive detailing of market dynamics. Bye Bye Banks? In ‘Bye Bye Banks?’ author James Haycock, Founder, and Managing Director of Adaptive Lab, along with Shane Richmond have given a clear message on the

The secret to consumer loyalty is ‘Relationship Banking’ and the mantra is ‘Serve first, Sell later’. ‘Platform customization‘ service is an effective way to attract and maintain more customers, as long as the costs associated can be controlled effectively. Designing the tailored solution that is ‘just right’ for the client gives them the proud feeling of ‘owning it’ rather than ‘using it’. With transactions, synonym to self-service, are increasingly moving online, the little remains of the customer service must be made even better. In this digital age, the brand and customer touch-points are the key selling points. Technology is increasingly changing consumers’ needs and expectations. Usually, e-commerce platforms are built around the idea that ‘one size fits all’. While this works for small businesses, anyone who is looking for ‘an out of the box’ solution should be looking out for ‘an out of the box’ platform too. So customization should be at the core of a flexible e-commerce platform that is ready to cater to the diverse business needs of ‘one and all’. Since there has been a drastic increase in digital payments and transactions post demonetization, many new users from both urban and semi-rural areas are adopting digital transactions. According to a white paper by ACI Worldwide along with AGS Transact Technologies (AGSTTL), the user base for digital transactions in India is currently close to 90 million with a projection of 300 million by 2020. This creates a constant demand for more and more reliable, holistic and scalable technology for digital payment platforms. Why is Customization of the FinTech Banking Platform Needed? While a lot of banking organizations have started re-shaping their payment systems and processes as per the users’ needs and payment behavior, many find mass penetration extremely challenging. The only solution is to build it customized and flexible to accommodate the growing demands of innovation and scalability. The service providers/ aggregators must be able to offer the bank and its client maximum return and full control over the financial architecture. This can only happen by means of a better understanding of the business policies and regulatory parameters. This would also bring all types of banking transactions onto one user-friendly platform which is secure and compliant with all regulations. It also provides many value-added services like payment of utility bills and recharges for its customers at one place. By enabling customization, banks can look at: Cutting operational costs by means of virtual and branchless transactions. Connect with a larger customer base and providing them with holistic banking experience virtually. Bypass the existing international payments network and thus resulting in more savings to both customers and the banks. Simplified procedures to save, secure and automatically share database across all the branches. Seamless transactions which give total control to the customers without the need for a bridge between the end-user and the banks. Improved saving and investment structure with minimal settlement time and cost. Needs vary from one person to other, and there is no ‘one size fits all’ rule. There are many things that you can achieve via customization of the platform that you won’t get in the general banking solutions. The main reason behind the necessity of customization is to be able to provide you with all the required features based on your needs and requirements. Key pointers to look for while customizing the platform B2B (agents/super agents), B2C (direct consumers) aspects need to take care of with a similar transaction flow. The solution should support all the interfaces such as Web, Mobile, USSD, SMS. It should have the capability to process online transactions as well as offline ((Especially in case of loans/insurance/tax/school fee collections, Pin based vouchers etc). It should be integrated with inbuilt business intelligence, analytics, and reporting modules with a real-time view for transaction monitoring purposes. Standard API should be used for other consumption networks to ride on the aggregated services. The solution should have the flexibility to integrate over multi-protocols viz. SOAP, ISO8583, HTTPS, file-based, Rest API, MT103, and MT104 etc. Multi-level authentication on the transaction (OTP/password/biometric) and encryption levels RSA2048, AES, SHA Hash etc should be supported. All business configurations like user roles, Access controls, commissions, discounts, products, services, accounting/reports, GLs and many more depending upon the customer’s requirements should be possible via the admin interface. Supports In-built customer support interfaces to record each customer query and resolutions. Also supports In-built auto-reconciliation feature for system transactions settlement with the 3rd party services providers. Should support system/transactions real-time monitoring with alarms configurations and different severity levels. The solution should have the capability to operate over cloud infra, the hybrid model or on-premise deployment. How are organizations getting benefitted from platform customization? With mobile technology becoming a huge facilitator to reach semi-urban and rural masses, connecting them with mobile banking would enable them to simplify the transactions. It will also facilitate digital transactions even from the unbanked segments of our economy promoting last-mile banking. Total control over financial management by monitoring dial-ups and directly attached devices. Bringing down the total ownership cost. Easy addition of POS device terminals with minimal or no downtime. Improve efficiency of operation through speeding time-to-market and increase revenue on a per-transaction basis. Make the payments more secure, reliable and simplified. Easy addition, edition and deletion of terminals and creating an omnichannel based transaction system. Gain a competitive edge by the ability to offer multi-currency dispensing and other value-added card features. Processing online as well as offline payment on a high-technology driven platform. Looking back, we at Teknospire, started our journey in 2015. Our flagship product “FinX” helps financial institutions to bring FinTech driven banking solution for the last mile. Its a complete package with well-integrated above-mentioned specifications and much more, and offers a secure and seamless banking experience. For more information please visit our website. Teknospire: Milestones Teknospire’s FinX FinX Digital Banking Solution Our FinX Agency Banking Suite enables a bank or financial institution to cost-effectively extend its branch network through the use of appointed and authorized banking agents. Another feather in our