GOI initiatives to boost Social and Financial Inclusion

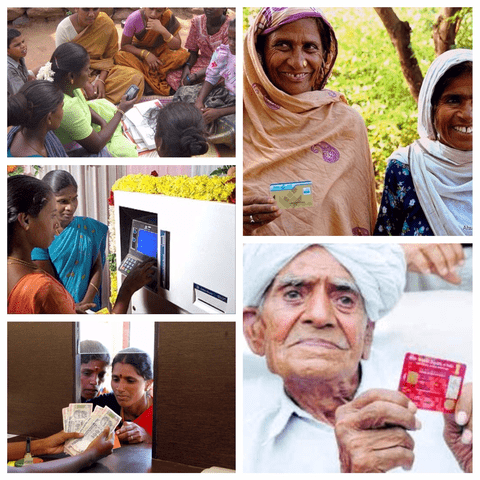

Hon’ble Indian Prime minister Mr. Narendra Modi said – I dream of Digital India where mobile and e-banking ensure financial inclusion. We might have heard many such quotes from our leaders, but what has been the ground reality? Has the government made any progress? What were the initiatives taken to boost social and financial inclusion? Demonetization? GST? MadeInIndia? JanDhanYojna Or DigitalIndia? Let’s dig in to explore – Images Source – Collage What is the Scope of Financial Inclusion? What all services could you think that needs to be included in Financial Inclusion? Deposits? Funds Transfer? Loans? While we do not have an official information on what all services need to be included in Financial Inclusion, but here are the basic banking services that could enable Social and Financial Inclusion – Access to Banks Accounts Instant Credits Instant micro loans for small business, education or agriculture Savings and Deposits Health Insurance Funds Transfer Investment or advisory services Pension for elderly individuals In general, any financial transaction through regulated channel as overall objective Challenges in Enabling Financial Inclusion in India India is the land of villages and farming, yet banks and banking haven’t reached around 19% of Indian population. Few of the challenges faced by Institutions, NGO’s, Fintech firms are – Missing Business model No digital reach and coverage Lower rate of education Setting up a bank branch locally is a costly affair Initiatives by GOI to Enable Social and Financial Inclusion Pradhan Mantri Jan Dhan Yojana One of the primary and significant schemes that allow individuals to open a bank account, basic banking no-frills account with nil/very low minimum balance as well as charges. Insurance and Pension Scheme GOI launched Pradhan Mantri Suraksha Bima Yojana (Accident Insurance), Atal Pension Yojana (Unorganized Sector) and Pradhan Mantri Jeevan Jyoti Yojana (Life Insurance), to enable social and economic security to the underprivileged sections of the society. MUDRA Bank to support Entrepreneurship Micro Units Development and Refinance Agency Bank (MUDRA Bank), launched in April 2015 provides loans at a low rate to enable enterprise for founders on rural/remote areas. Stand up India Another scheme initiated by GOI, each branch of public sector banks need to support one entrepreneur from Women and minority society. Direct Transfer of Government Benefits As we are witnessing LPG subsidies now getting credited directly to your accounts, on similar lines through Pahal Scheme GOI is keen to transfer grants and funds directly to beneficiaries account, removing the middle layer. Micro finance companies[MFC] MFC that provide micro loans to farmers, stall owners, women’s help in structuring the financial loan service and helping people from the money lenders debt trap. GST As cleartax defines Goods & Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that will be levied on every value addition. GST also brings in the benefits of enabling financial inclusion by – Simplifying the Tax We all know that apart from CA’s, accountants and some learned, tax and its rules are still a bouncer to many of us. We have seen a debate on why the restaurant charged a VAT or service charge or service tax on my bill? Or have we not witnessed a Tv commercial showing how a farmer from his mobile phone ordered seeds for his farming? Do you think he would ever understand why he has to pay VAT? or if stays in Maharashtra why he has to pay Octroi ? Or how about a rural individual selling his handcrafted products to Maharashtra, would have a tough time to know why while processing in Pune Octroi charges applies. With uniform tax system, it’s easy to learning making it simpler for individuals to absorb it. One System Digitization Digitization automation demands one system that could track the tax channels. With multiple tax laws integrating them into one system is tough. Hence many times we have seen people ignoring paying the tax because there was no system to track or pay it outside the formal system via cash. With solutions available now on mobile devices, it’s easy for any rural person to track down his selling/purchasing in all cases. Unorganized Sectors to be Structured with no middlemen With initiatives like Digital India, Aadhaar linking to Bank accounts, PF and PAN cards, the GOI is trying to tie individuals to one identity. Taking a step further with the introduction of GST linking of the identification to tax system would be easy for small businesses and unorganized sector to follow formal tax rule. Just imagine a potter trying to sell his products across pan-India would now have a single identity card linked to his Bank account and GST Registration. Standard Pricing With formal tax-system retailers cannot mark product pricing as per their wish. GST also has an anti-profiteering clause, that mandates all businesses to pass on the benefits to the end customers. With such initiatives, one could expect products to be available and consumed in remote areas enhancing their standard of living. Use of technology With the ease of technology and availability of mobile phones – solutions like Agent banking are enabling financial inclusion in the remotest areas of the developing countries like India, Bangladesh, and Zimbabwe. General Purpose Credit Card [GCC] GCC allows the holder with a credit facility of up to 25,000 in rural and semi-urban bank branches. The primary objective of this scheme is to provide instant and hassle-free credit to its customers. How Teknospire a fintech firm is enabling Financial Inclusion in India Teknospire with its tagline Inspiring technologies for better living is a proud contributor to help in financial Inclusion. With its range of Fintech and HealthTech solutions to provide secure Agent Banking or Mobile Money suite or to credit grants to beneficiaries account , Teknospire is making it possible. GOI is putting extra efforts to bring the change, however firms like Teknospire are adding value to these plans and making execution a possibility with our skilled team and latest technology. The financial architecture in place thanks to GOI; we have the